Global Wood Pellet Markets Soar in 2018

Global Pellet Trade in 2018

Wood Pellets Green Fuel

Bulk Wood Pellet

In terms of growth and pricing, 2018 was one of the strongest years for the global wood pellet market in quite some time.

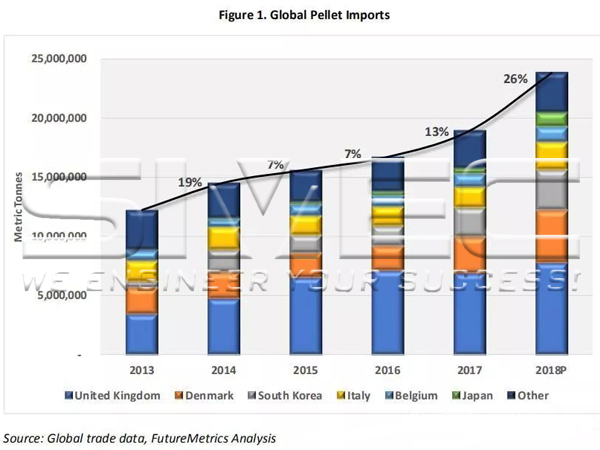

From 2014 to 2016 the growth in global wood pellet trade slowed to 7% per year, accompanied by a low pricing environment and limited capacity expansion. In 2017 market conditions greatly improved and global trade increased 13% to 18.9 million tonnes. That market improvement continued in full force through 2018 as the growth in global pellet trade accelerated to 26%. FutureMetrics projects 2018 pellet trade will have increased to 23.8 million tonnes in 2018 up from 18.9 million tonnes in 2017 (Figure 1). That growth is primarily fueled by increased demand in the UK, Denmark, South Korea and Japan.

Figure 1. Global Pellet Imports

This white paper provides and overview of global pellet trade in 2018.Wood Pellets Green Fuel

Bulk Wood Pellet

From 2014 to 2016 the growth in global wood pellet trade slowed to 7% per year, accompanied by a low pricing environment and limited capacity expansion. In 2017 market conditions greatly improved and global trade increased 13% to 18.9 million tonnes. That market improvement continued in full force through 2018 as the growth in global pellet trade accelerated to 26%. FutureMetrics projects 2018 pellet trade will have increased to 23.8 million tonnes in 2018 up from 18.9 million tonnes in 2017 (Figure 1). That growth is primarily fueled by increased demand in the UK, Denmark, South Korea and Japan.

Figure 1. Global Pellet Imports

United Kingdom

In 2018, UK pellet demand increased with the commissioning of EPH’s 396 MW Lynemouth Power Station conversion and the conversion of a 4th unit at the Drax Power Station. 2019 growth will be primarily driven by a ramp up to full operation at Lynemouth and increased availability at the Drax power station. In 2020 UK demandwill increase again with the scheduled commissioning of MGT’s 299MW Teeside CHP plant.

In 2018, UK pellet demand increased with the commissioning of EPH’s 396 MW Lynemouth Power Station conversion and the conversion of a 4th unit at the Drax Power Station. 2019 growth will be primarily driven by a ramp up to full operation at Lynemouth and increased availability at the Drax power station. In 2020 UK demandwill increase again with the scheduled commissioning of MGT’s 299MW Teeside CHP plant.

Denmark

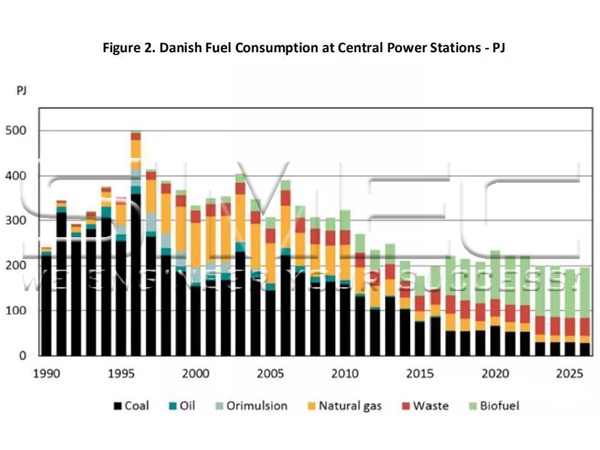

The consumption of wood pellets in Denmark ranges from individual appliance users to small district heating plants to industrial scale CHP facilities. Much of the recent growth has come from the conversion of large central power stations from coal to biomass. Denmark has 9 central power stations, several of which have already been converted to biomass. Denmark has committed to phasing out coal by 2020, which will likely mean several more unit conversions. However, the additional facilities will likely be converted to wood chips or other forms of lower value waste. The majority of future wood pellets demand growth in Denmark will come from smaller-scale district heating and continued growth in the residential sector.

Figure 2. Danish Fuel Consumption at Central Power Stations - PJ

Belgium

The consumption of wood pellets in Denmark ranges from individual appliance users to small district heating plants to industrial scale CHP facilities. Much of the recent growth has come from the conversion of large central power stations from coal to biomass. Denmark has 9 central power stations, several of which have already been converted to biomass. Denmark has committed to phasing out coal by 2020, which will likely mean several more unit conversions. However, the additional facilities will likely be converted to wood chips or other forms of lower value waste. The majority of future wood pellets demand growth in Denmark will come from smaller-scale district heating and continued growth in the residential sector.

Figure 2. Danish Fuel Consumption at Central Power Stations - PJ

Belgium

Belgium’s industrial wood pellet demand has remained relatively stable over the last several years as there are two power stations fueled by wood pellets, both operated by Engie Electrabel, the 80 MW Les Awirs and the 205 MW Max Green power station. The increase in pellet imports seen in 2018 is likely reflective of a higher capacity factor at the biomass plants due to strong electricity markets, and improved conditions in the domestic heating market.

Netherlands

The Netherlands has a history as a major market for industrial wood pellets. In 2010, the Netherlands was the biggest market for industrial wood pellets – used for co-firing to meet renewable energy goals. The market rapidly declined when a new renewable energy subsidy scheme was introduced in 2012. The scheme required the development of new sustainability standards before biomass co-firing could qualify for subsidies. In 2016, subsidies were awarded for co-firing at 4 power plants, RWE’s Amer and Eemshaven power stations, Engie Rotterdam and Uniper Maasvlakte 3 (MPP3). Unit 9 at the Amer power station, which had previously co-fired under the old subsidy scheme, resumed co-firing of significant amounts of wood pellets in the 4th quarter of 2018. The other plants will likely begin co-firing in 2019 and 2020, making the Netherlands once again a major market for industrial wood pellets.

The Netherlands has a history as a major market for industrial wood pellets. In 2010, the Netherlands was the biggest market for industrial wood pellets – used for co-firing to meet renewable energy goals. The market rapidly declined when a new renewable energy subsidy scheme was introduced in 2012. The scheme required the development of new sustainability standards before biomass co-firing could qualify for subsidies. In 2016, subsidies were awarded for co-firing at 4 power plants, RWE’s Amer and Eemshaven power stations, Engie Rotterdam and Uniper Maasvlakte 3 (MPP3). Unit 9 at the Amer power station, which had previously co-fired under the old subsidy scheme, resumed co-firing of significant amounts of wood pellets in the 4th quarter of 2018. The other plants will likely begin co-firing in 2019 and 2020, making the Netherlands once again a major market for industrial wood pellets.

Italy

Italy is unique among major importers of wood pellets in that the Italian pellet market is primarily for home heating as opposed to industrial use. Italian pellet imports were well below highs seen in 2014 due to warm winters and lower prices for competing fuels like heating oil. Volumes recovered significantly in 2017 and, in the first eight months of the year, 2018 imports are 29% higher and on pace to break previous records set in 2014.

Other Europe

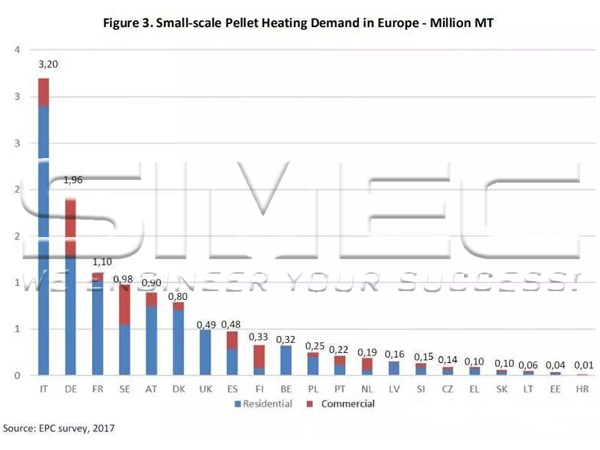

There are several major pellet markets in the EU that are not represented in trade data because they are primarily self-sufficient in producing the majority of pellets that they consume. For domestic heating, these include Germany, estimated at ~ 2 million tonnes, and France, Austria and Sweden, estimated at ~1 million tonnes each (Figure 3). Sweden also has a significant industrial market at small and mid-sized heating and CHP plants. We expect continued modest growth in these and other smaller heating markets in the coming years. Heating markets are extremely sensitive to external factors like the price of competing fuels and weather.

Figure 3. Small-scale Pellet Heating Demand in Europe - Million MT

Figure 3. Small-scale Pellet Heating Demand in Europe - Million MT

Japan

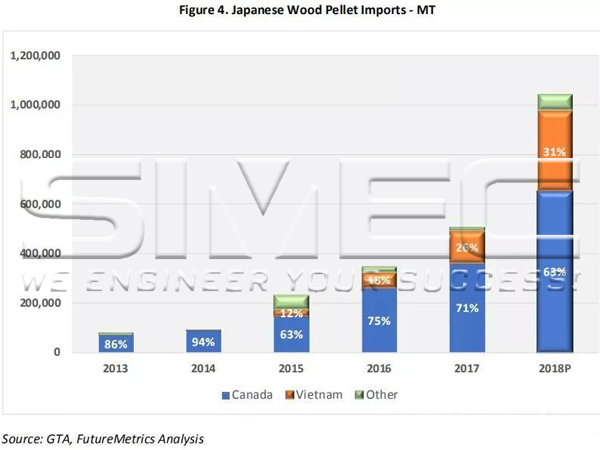

Japanese wood pellet imports are on pace to exceed 1 million tonnes in 2018, approximately double the amount of imports from 2017. Through the first 3 quarters of 2018, 63% of Japan’s wood pellet imports came from Canada and 31% from Vietnam. Due to the fixed price and long contract length of the Feed-in-Tariff subsidy that supports renewable energy in Japan, long term contracts from strong counter-parties, like those in Canada and the USA are the preferred form of procuring wood pellets for most Japanese buyers. We expect to see continued rapid expansion in Japanese wood pellet imports in the years to come. Our full detailed analysis on Japan is available in FutureMetrics’ 2018 Japanese Biomass Outlook which will be updated again in early 2019.

Figure 4. Japanese Wood Pellet Imports - MT

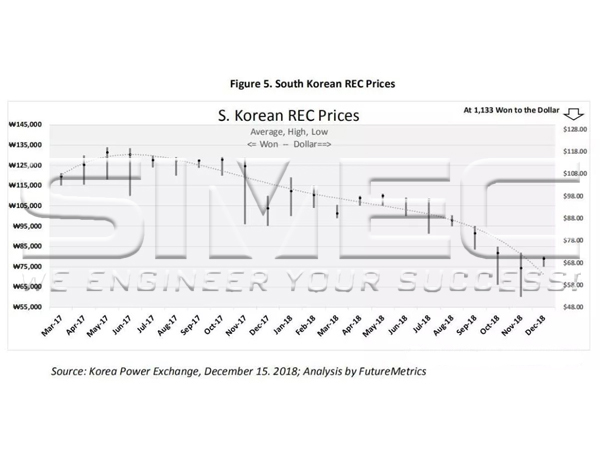

Figure 5. South Korean REC Prices

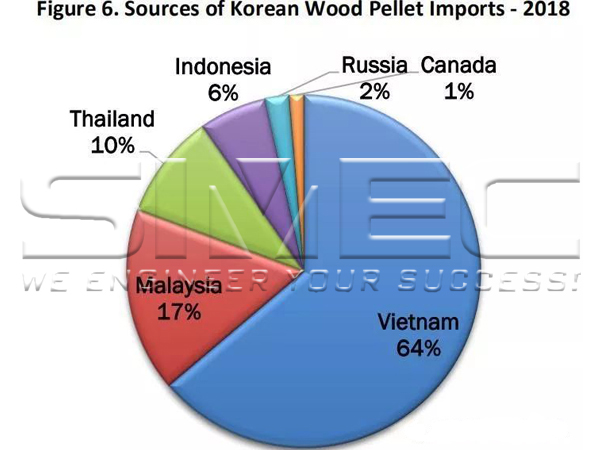

Figure 6. Sources of Korean Wood Pellet Imports - 2018

In South Korea, renewable energy is promoted by an RPS that requires an increasing amount of their energy to come from renewable sources. Tradable Renewable Energy Certificates (RECs) are used to demonstrate compliance. Utilities have three ways of meeting the RPS: produce RECs themselves, purchase RECs on an exchange, or pay a fine equal to 150% of the average REC price during the year. Due to uncertainty regarding the value of RECs, the price of power and the price of pellets, South Korean buyers have a more difficult time entering in to long-term contracts. Nevertheless, there have been instances of successful contract negotiations with North American producers, particularly with dedicated biomass plants (as opposed to major utilities co-firing at coal stations).

Conclusions

Pellet markets are on a robust upward trend with continued growth in Europe and a maturing set of trade flows in the Pacific basin. In addition, producers have taken a more cautious approach to development over the last several years, allowing supply and demand to move towards re-alignment. While there are still risks, like policy uncertainty, competing fuel prices, and dependence on weather, overall the industry is in a very strong position moving in to the early 2020s.

Figure 4. Japanese Wood Pellet Imports - MT

South Korea

While the Japanese market has captured most of the attention of North American producers and European buyers of wood pellets, South Korea has quietly become the 2nd or 3rd biggest wood pellet market in the world (after the UK and very close to Denmark). However, unlike Japanese buyers who look for stability and long-term contracts. Most of the pellets currently being traded into South Korea are on a short-term or spot basis. South Korean utilities, who co-fire wood pellets to help meet their renewable portfolio standards (RPS), are much more price sensitive due to the nature of their business.

While the Japanese market has captured most of the attention of North American producers and European buyers of wood pellets, South Korea has quietly become the 2nd or 3rd biggest wood pellet market in the world (after the UK and very close to Denmark). However, unlike Japanese buyers who look for stability and long-term contracts. Most of the pellets currently being traded into South Korea are on a short-term or spot basis. South Korean utilities, who co-fire wood pellets to help meet their renewable portfolio standards (RPS), are much more price sensitive due to the nature of their business.

Figure 5. South Korean REC Prices

South Korean demand is largely responsible for the rapid development of wood pellet production capacity in Southeast Asia. In 2018, South Korea’s wood pellet imports are projected to reach 3.4 million tonnes, with more than 95% of that volume coming from Southeast Asia (Figure 6).

Figure 6. Sources of Korean Wood Pellet Imports - 2018

Conclusions

Pellet markets are on a robust upward trend with continued growth in Europe and a maturing set of trade flows in the Pacific basin. In addition, producers have taken a more cautious approach to development over the last several years, allowing supply and demand to move towards re-alignment. While there are still risks, like policy uncertainty, competing fuel prices, and dependence on weather, overall the industry is in a very strong position moving in to the early 2020s.